Most Toronto Homeowners

Pay More for

Their Mortgage

Than They Need To

A smarter mortgage approach that helps you reduce debt, improve cash flow, and pay less for your home —

without having to figure it out yourself.

Adam Stapley | Mortgage Broker Integrity Tree Financial (Lic. #12963)

Without a Strategic Review, Renewing Your Mortgage Can Cost More

Most homeowners set up their mortgage once, then automatically renew it when the term expires.

The lender sends a renewal offer, the rate seems fair, and the paperwork is signed without much thought.

But over time, rates change, debts grow, and finances evolve.

Without a comprehensive review of your mortgage and overall financial picture, it’s easy to pay more interest than necessary and miss opportunities to improve cash flow.

A mortgage shouldn’t just be renewed — it should be reviewed, adjusted and aligned with your long-term goals.

When approached strategically and reviewed regularly, a mortgage can become a powerful tool for reducing interest costs and strengthening your overall financial position.

The Right Mortgage Strategy Matters More Than Rate

Most homeowners are told to focus on getting the lowest rate possible.

But your interest rate alone doesn’t determine how much your home will ultimately cost you.

What matters just as much — and often more — is how your mortgage is set up, how it interacts with your other debts, and whether it’s reviewed as your financial life evolves.

The "lowest" rate on the wrong structure today can cost more over time.

Without a clear strategy, it’s easy to pay unnecessary interest, carry high-interest debt longer than needed, and miss opportunities to strengthen your cash flow.

Our goal isn’t just to secure you a mortgage.

It’s to design a mortgage that actively reduces your total cost of borrowing — not just today, but as your finances and goals change over time.

The Rolling Renewal Strategy

The Best Time to Plan Your Renewal Isn’t at Renewal!

Most homeowners wait for their bank to send them their mortgage renewal offer.

By then, you're already too late.

The most strategic moves that save you thousands of dollars start 8 - 12 months before your mortgage matures.

That's the idea behind the Rolling Renewal Strategy.

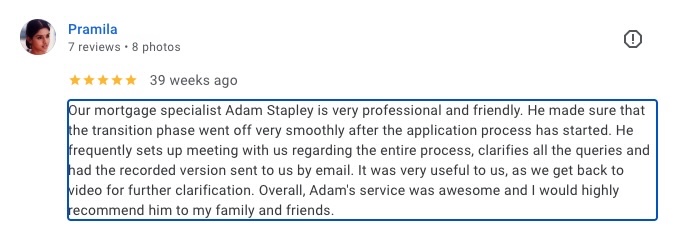

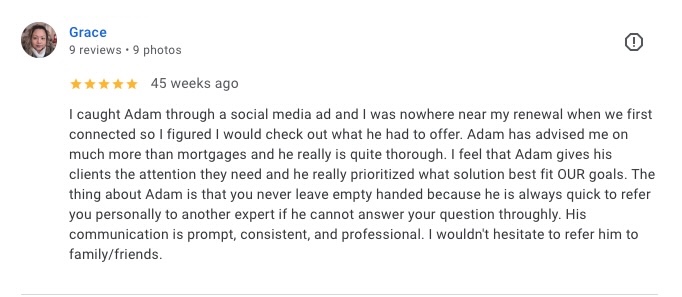

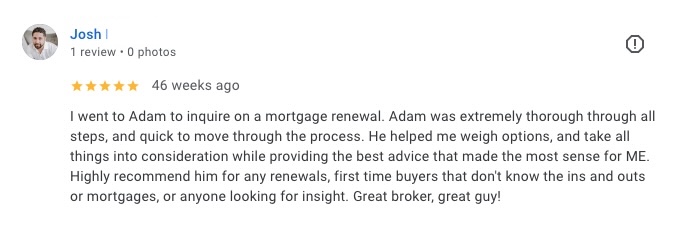

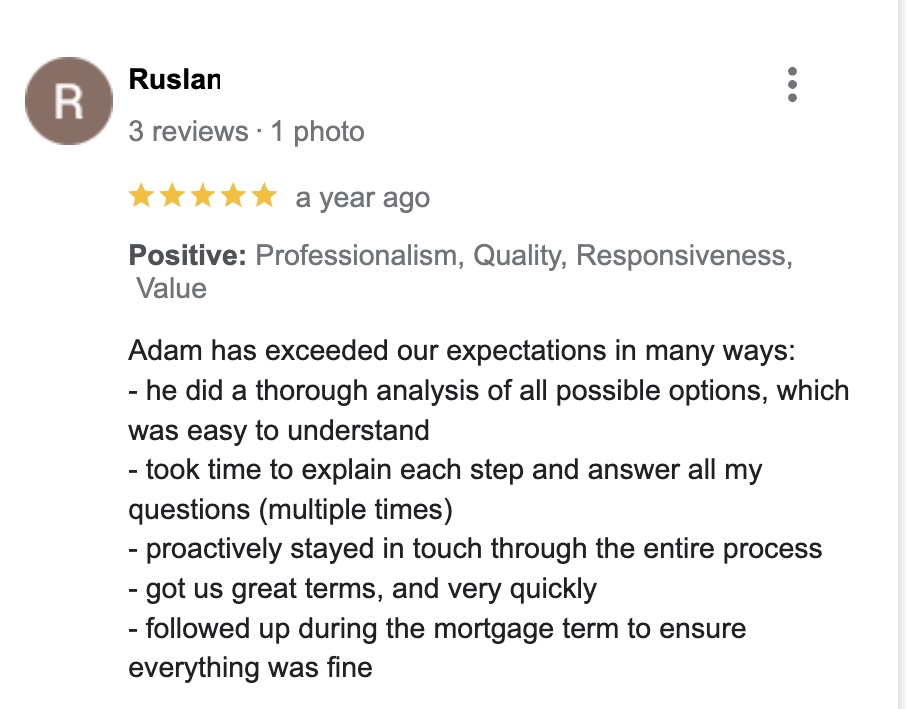

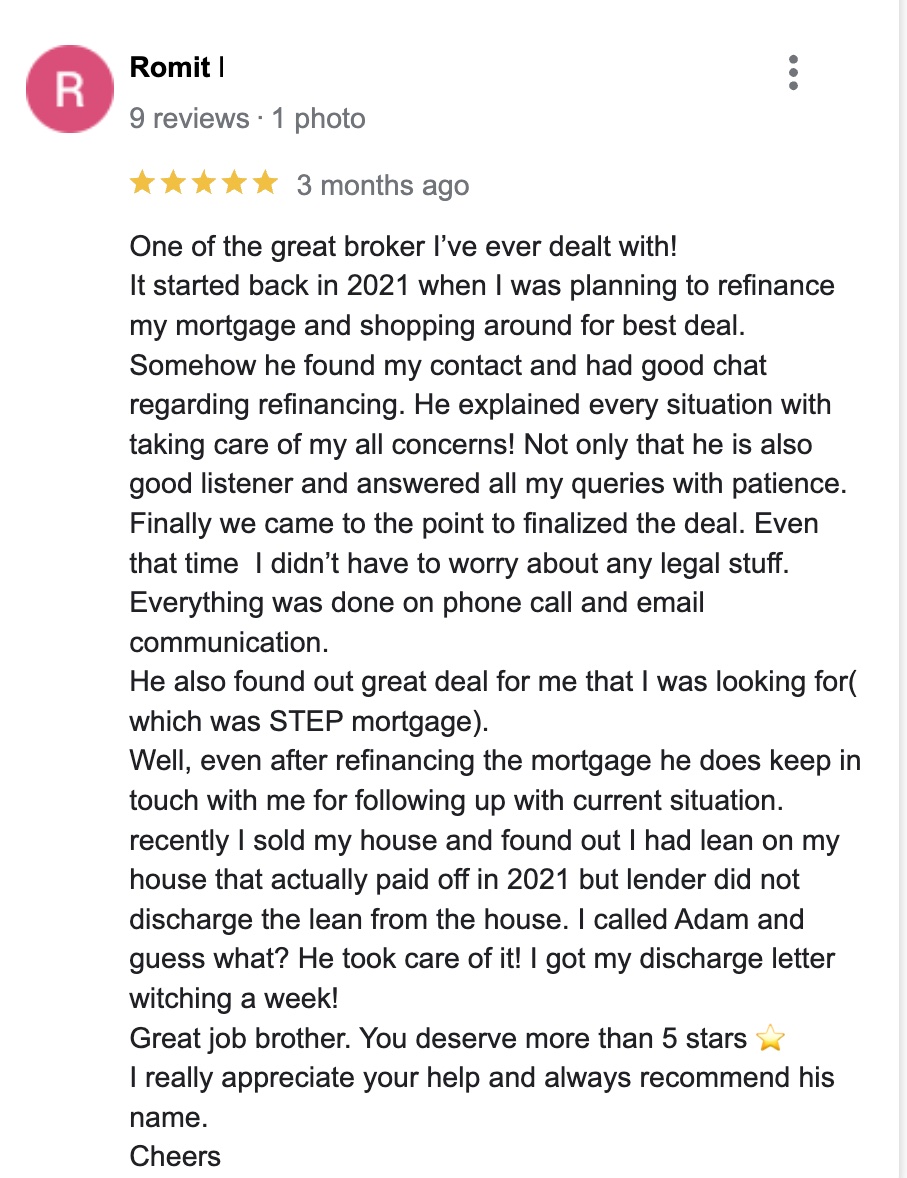

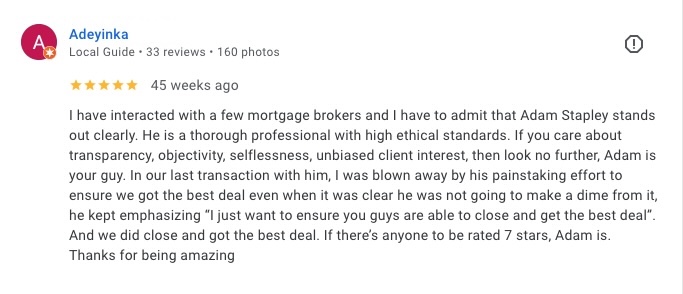

Trusted by Homeowners Accross Toronto

50+ Five-Star Google Reviews

Meet Adam

Mortgage Broker

I help Toronto homeowners like you pay less for their homes.

By building smart, long-term mortgage strategies, you'll save interest and minimize your mortgage's impact on cash flow.

Working with me gives you access to monthly monitoring, bi-annual reviews and advanced renewal strategies all designed to keep more money in your pocket, not your bank's.

What Happens When You Book a Call

Step 1

Book a 20-minute discovery call

Step 2

Review your current mortgage & goals

Step 3

Identify opportunities to reduce costs

Step 4

Build a clear mortgage strategy